Instead, it indicates that the project does not return the discount rate used for the analysis. In this example, the net cash inflows from the Diamond LX model have a slightly higher net present value than the net cash inflows from the VIP Express model. So, the company must decide whether or not to invest in the machine by comparing the initial investment to the expected future cash flows. If the expected cash flow is greater than the initial investment, then logically, the company should invest in the machine.

What Is the Difference Between Capital Budgeting and Working Capital Management?

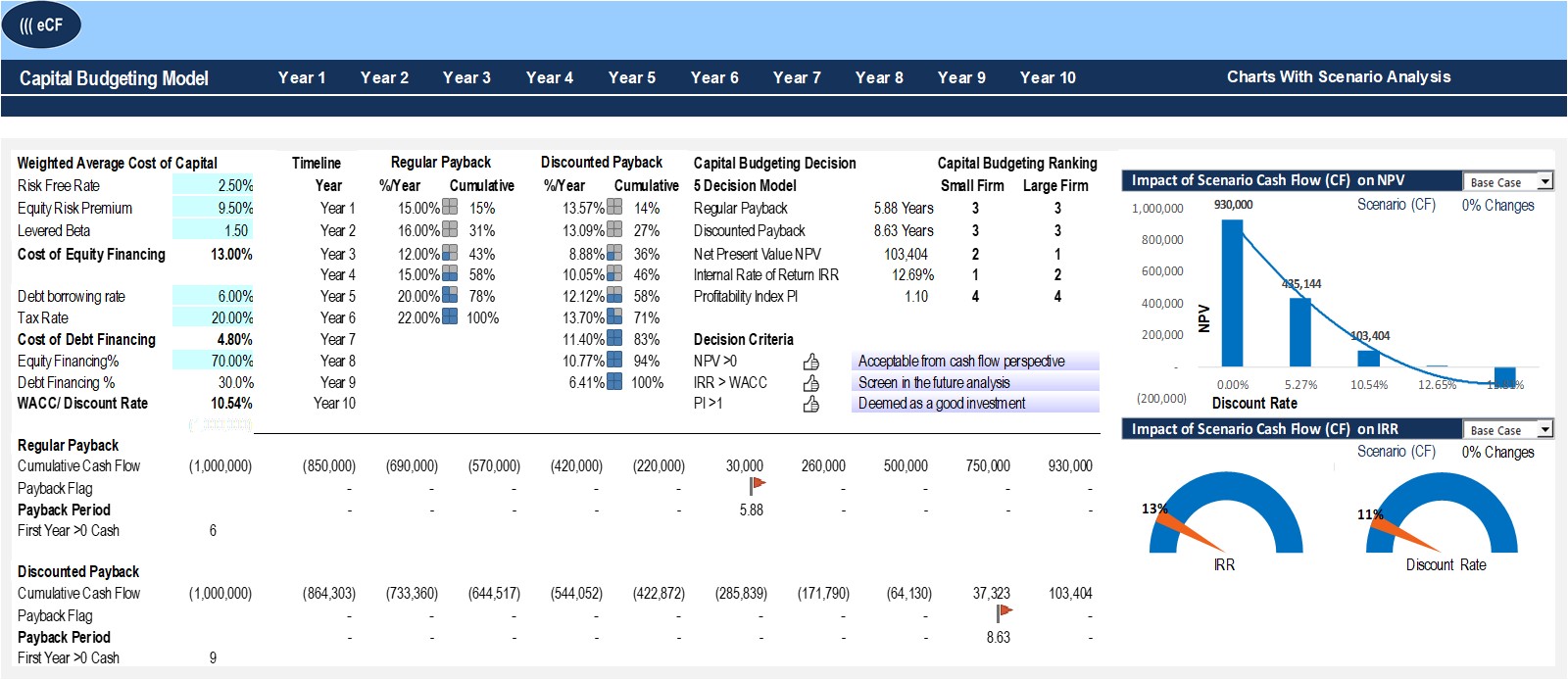

This tool can identify the investments that meet a specific minimum rate of return. This is a simple way of assessing the profitability of an investment based on financial data. The higher the result, the more likely a project will be profitable. The primary objective of capital budgeting is to maximize shareholder wealth. You want to ensure that you’re choosing projects that are expected to raise good profits.

- Inflation typically occurs gradually over a long period of time, so it is often ignored in capital budgeting decisions.

- If their goal is to be number one in their industry, capital budgeting can help them invest in projects with that goal in mind.

- Many use existing accounting software to help track and manage projects and investments, while others stick to more conventional methods of spreadsheets.

- In this step we will look at all of the projects, and determine whether they meet the company’s basic guidelines for consideration.

- This way, the company can identify gaps in one analysis or consider implications across methods that it would not have otherwise thought about.

- A zero net present value means that the return on the investment equals the discount rate.

Factors Affecting Capital Budgeting

This chapter discusses four methods for making capital budgeting decisions—the payback period method, the simple rate of return method, the internal rate of return method, and the net present value method. Through capital budgeting, companies can determine whether their potential investments will likely be profitable and worthwhile. The second step, exploring resource limitations, evaluates the company’s ability to invest in capital expenditures given the availability of funds and time. Sometimes a company may have enough resources to cover capital investments in many projects. Many times, however, they only have enough resources to invest in a limited number of opportunities.

3 Explain the Time Value of Money and Calculate Present and Future Values of Lump Sums and Annuities

The Diamond LX discount factor is 6.814 taken from row 12, 10% column. The VIP Express discount factor is 6.145 taken from row 10, 10% column. The Diamond LX and VIP Express models have the same types of cash inflows/outflows–investment required, annual net cash inflows, and the salvage value at the end of the useful life.

It is a challenging task for management to make a judicious decision regarding capital expenditure (i.e., investment in fixed assets). The objective of capital budgeting is to rank the various investment opportunities according to the expected earnings they will yield. Companies are often in a position where capital is limited and decisions are mutually exclusive. Management usually must make decisions on where to allocate resources, capital, and labor hours.

How Are Capital Budgets Different From Operational Budgets?

This way, the company can identify gaps in one analysis or consider implications across methods that it would not have otherwise thought about. Every year, companies often communicate between departments and rely on financial leadership to help prepare annual or long-term budgets. These budgets are often operational, outlining how the company’s revenue and expenses will shape up over the subsequent 12 months. As a result, payback analysis is not considered a true measure of how profitable a project is but instead provides a rough estimate of how quickly an initial investment can be recouped. It allows companies to conduct a thorough and systematic assessment of various investment opportunities, aiding in informed decision-making. Capital budgeting employs various techniques like net present value (NPV) and internal rate of return (IRR) to assess the profitability of long-term investments.

IRR helps businesses understand just how profitable their investment could be. This enables you to find the rate at which the investment breaks even—the “golden rate.” The higher the IRR, the more lucrative the investment. The process involves a comparison of Financial vs. Economic rate of return, Internal Rate of Return (IRR), Net Present Value (NPV), and Profitability Index (PI). Choosing the most profitable capital expenditure proposal is a key function of a company’s financial manager. The total capital (long/short term) of a company is used in fixed assets and current assets of the firm.

For this reason, managers must be able to evaluate the alternatives and select the project that offers the most benefit to the organization. The ability to choose appropriate capital investments is an essential component of an organization’s long-term financial health and stability. In this step we will look at all of the projects, and determine whether they meet the company’s basic guidelines for consideration. Our company, may for example, require a 20% rate of return on a new investment before it will even be considered as an option. Once we screen all of the potential options, if any meet this guideline, we can move on the the preference decision. Such an error violates one of the fundamental principles of finance.

Project managers can use DCF to help them decide which of the several competing projects are worth pursuing at the moment. Finance Strategists has an advertising relationship with some of the companies included on this website. We may earn a commission when you click on a link or make a purchase through the links on our site. All of our content is based on objective analysis, and the opinions are our own. Approval of capital projects in principle does not provide authority to proceed. Some worthwhile projects may not be approved because funds are not available.

The primary goals of budgeting encompass planning, controlling, and evaluating performance. Firstly, it involves the creation of a comprehensive plan outlining the allocation of conversion method of single entry system or transaction approach resources. Since the Profitability Index is greater than one, the investment is likely to be profitable. The higher this figure, the more attractive the investment will be.